Jordan Belfort talks about Money Often, But This Time, It’s For Real.

“It’s the most lucrative investment for the average person.”

The cost of wasted potential can be catastrophic.

Piers Morgan once said:

“The people who knew Jordan Belfort in his heyday said he was that good as a trader, and with money, he would’ve been a billionaire without the criminal activity.”

He never needed to cross that line.

Belfort hit rock bottom when he lost his family, wealth, and freedom by misdirecting his remarkable sales and money management skills.

Jordan Belfort says himself that it’s true:

“The sad part is that if I hadn’t taken that left turn to Albuquerque, so to speak, I would have made $10 or $20 billion because I would’ve hit the internet bubble and taken companies public. One of the biggest mistakes people make is they cut a few corners to make money a little quicker, but big money takes time, and you can’t cut corners.”

Like many, I got hooked on the story through the film The Wolf of Wall Street, in which Leonardo DiCaprio depicts the entire story. Dramatised for Hollywood, of course.

Belfort operated a penny-stock scam through his brokerage firm, Stratton Oakmont. The firm used aggressive sales techniques to defraud investors.

Strangely, the scene that really sticks with me is the Aerotyne Phone Sale. Leonardo DiCaprio walks into The Investor Centre, right into the chaos of pink sheet trading.

It’s a complete rookie show.

The sales centre manager sits him down and says:

“Aerotyne is a very hot stock. They’re just a couple of brothers making radar detectors out of their garage. When you call the company, their mom Dorothy answers.”

Dicaprio responds with: “Six cents a share — who buys this crap?”.

Manager answers: “Mostly schmucks”.

When DiCaprio, playing Belfort, kicks off his new gig at the centre, he cold calls an unsuspecting guy named John to sell Aerotyne stock, and the deception is ruthless.

Leonardo Dicaprio — Source

“John, you requested information on penny stocks with huge upside potential with very little downside risk.

Something just came across my desk, John. It is the best thing I’ve seen in the last six months. Aerotyne International is a cutting-edge, high-tech firm out of the Midwest awaiting imminent patent approval on the next generation of radar detectors with huge military and civilian applications.

John, the stock trades over the counter at 10 cents a share, and John, our analysts indicated it could go a heck of a lot higher than that. Profit on a mere $6,000 investment would be upwards of $60,000.”

John: “Jesus, that’s my mortgage, man. I could pay off my mortgage.”

The trade locks in, and the whole office is left stunned.

The rest of the film follows a similar theme of deception and carnage, depicting out-of-control drug binges, hookers and office scenes that resemble a frat party.

It’s not lost on me that many lives were destroyed behind the Hollywood adaptation and the story’s sensationalism. No matter how great Leonardo DiCaprio acted or how lavish Belfort’s lifestyle was, the victims suffered the most.

Belfort was released from prison in April 2008 after being convicted of defrauding 1,513 investors out of over US$200 million, which included his ex-wife Nadine and even his own children.

His sentence included four years behind bars, 22 months of which he served, and an obligation to pay 50% of his gross income to victims following his release.

2014, during a global speaking tour, Belfort said he hoped to earn “over $100 million” by giving speeches about his story because “Once everyone is paid back, believe me, I will feel a lot better.”

Now, on his path to redemption, Belfort shares insights on where to invest your money.

It’s something very few people expected to hear.

Every investor should do this.

I’m as guilty as the next person getting caught up in the excitement of these tech companies making headlines and posting huge profits.

Maybe for good reason.

Jordan Belfort’s investment advice is surprisingly simple — it’s almost dull. He says:

“Park your money in the S&P500 and forget about it. It’s the most lucrative investment for the average person.”

I never thought I’d hear those words from a man who orchestrated pump-and-dump schemes for quick cash, but what he’s saying makes a lot of sense.

Even The Oracle of Omaha advised investors in his Berkshire Hathaway Letter that his wife should put most of his wealth into the S&P 500 after his death.

This came from a man who outpaced the market by making 3,787,464% gains with his Berkshire Hathaway stock vs the 24,708% increase during the same period of the S&P500.

“My advice to the trustee could not be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund.

I believe the trust’s long-term results from this policy will be superior to those attained by most investors — whether pension funds, institutions or individuals — who employ high-fee managers,”

Just buy and hold.

Few people can beat the S&P500 consistently.

Belfort says for the fund managers that can — “Guess what, they’re not going to take your money. They are the rock stars of the hedge fund world. Then you have the rest of them that underperform.”

He says instead of rotating in and out of single stocks and trying to time the market, bet on the entire pie.

It’s practically an open secret that no one seems to follow.

Jordan Belfort — Source

“If you simply put your money in the S&P 500 and hold it for the long term, not for one year, not even three years. If you look at the long-term chart over any ten years and then as you go to 20 years and 30 years, if you buy it and hold it, you will outperform 99.9% of all the hedge funds and mutual funds out there.”

Here’s what the data says

I did some digging into the S&P 500.

Firstly, the S&P index tracks the performance of 500 large companies listed on stock exchanges in the United States.

Macro investors, traders and politicians often use the S&P500 as a benchmark for the overall health of the U.S. stock market.

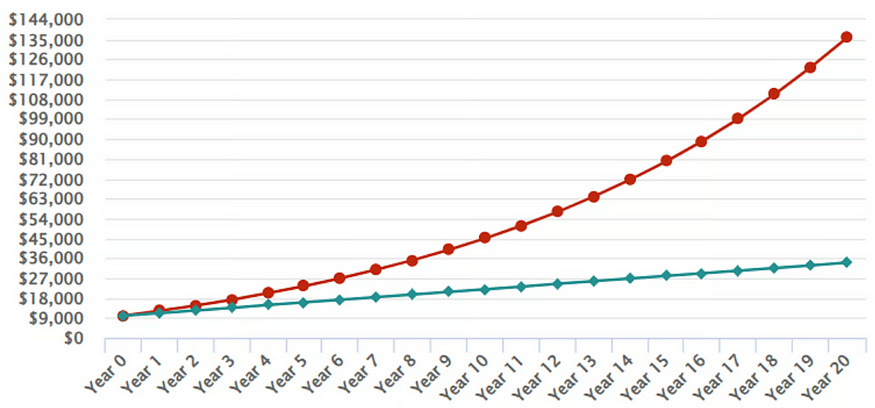

If you had consistently invested over the last 20 years, the S&P500 would have given you, on average, a 9.69% return. Assuming you reinvested dividends and did not adjust for inflation, which is currently 3%

Let’s crunch the numbers.

Assuming the index averages a 10% annual return, you started with a $10,000 investment 20 years ago. By consistently adding $100 monthly, you’d now be looking at $136,000.

You’ll have a total cost basis of $34,000 over 20 years, making you over $100k with zero brain power or professional investment knowledge.

Not everyone agrees.

We live in an exponential age of technology.

Investing can now be done with a click of a button and is somewhat of a cultural phenomenon — but to quote a famous macro investor, Raoul Pal,

“The S&P 500 isn’t the fastest horse in the race.”

Pals’ thesis is that liquidity is the biggest driver of asset prices and that the S&P500 is correlated to M2 money supply.

“What I found in my work was that liquidity was essentially everything. Only two markets were in a secular trend: technology and crypto. Everything else basically reflected the debasement of currency of about 8% a year. So, liquidity is the key driver and the most important thing for us to understand.”

What he says is while inflation might now be down at 3%, money printing is increasing at a rate of 8%, which is debasing our purchasing power, so you have a hurdle rate of 11%

Pal says you might feel richer on a nominal basis investing in the S&P500 when it increases, but you’re not.

“It’s the actual debasement of currency that makes assets look like they’re going up — so the Venezuelan stock market, if you ever see a chart, looks like it goes vertical. Looks like the best-performing stock market in the world, right? Of course, when you put it in the Venezuelan bolivar, it’s down 90%. Right, it’s because they’ve been devaluing the bolivar.”

Pal says the same is happening in the U.S. on a less extreme level. People see their asset prices increase when, in reality, they need to factor in the debasement of their purchasing power into the equation.

When you do, you find the S&P stays stagnant against inflation and money printing.

Final Thoughts.

I disagree that an index fund or the S&P500 “is the most lucrative investment for the average person”.

It’s a suboptimal bet for the average person.

Finance guru Dave Ramsey also advocates for this passive investing approach, suggesting you go for the whole market.

It doesn’t make sense to me.

Diversification is dead if all assets are correlated with money printing minus technology and crypto, which is outperforming.

I agree with Pals take that you’ll just be treading water. People are getting screwed so badly that they can’t even invest, which is why they head down to the casino of Meme coins.

It’s their only option.

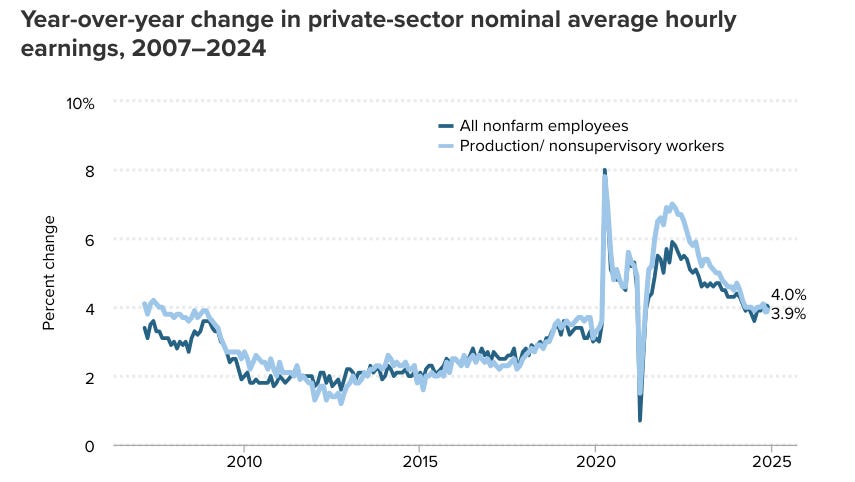

Since 2007, nominal wage growth has increased by only 4.2%, which is nowhere near the 8% debasement rate. So you earn less, and your money is worth less.

Why on earth would I tie up my money for 25 years in an investment that moves slower than a glacier?

While I disagree — it’s a surprisingly honest lesson.

One I never expected from Jordan Belfort.

If you found value in this newsletter, feel free to share it! Or, if you’re ready to level up, upgrading to a higher-tier membership unlocks a 1-2-1 call with me and plenty of other perks.